Investors are wondering why bond returns were down double digits in 2022. The reason is simple: rates are rising faster than any other time since 1988.

It is important to note that bonds are different than stocks. A bond issued by a company or municipality must continue to pay the investor coupon payments plus the stated future value of the bond at maturity unless the company/municipality defaults on the debt.

It is very rare for many types of bonds to default. For example, the historical default rate since 1970 for investment-grade municipal bonds is 0.1%. As a result, any current losses on bonds will likely be recovered as the bond gets closer to maturity. For those invested in bond funds, the manager may sell bonds prior to maturity but only if they see greater opportunities elsewhere. In other words, the ‘losses’ many are seeing in their portfolios are highly probable to be only temporary (unless a sale is made).

Should I Sell My Bonds Now (2023)?

Unless there is a change in your circumstances, we believe investors should continue to hold onto their bonds for the following reasons:

- The bonds will mature at par value, meaning you will receive the face value of the bond at maturity, so present-day dips in value are only temporary

- Coupon payments are still being made

- Yield is locked in at purchase, with the opportunity to reinvest coupon and maturing bonds at higher yields

How to Calculate Bond Price Changes

Assuming no other external factors, calculating bond value changes is straightforward. For simplicity, if rates rise 1% and a bond matures in 4 years (technically if its duration is 4 years), then the bond value declines by 4% and vice versa.

Additionally, a rate increase from 0% to 1% is more impactful to bond values than a rate increase from 4% to 5% because it is a 100% increase versus a 20% increase in rates. The reason for this inverse relationship is that when interest rates increase, new bonds offer higher coupon payments. Existing bonds with lower coupon payments must decline in price in order to be worthwhile investments to would-be buyers.

In the real world, bond yields already reflect the current market’s expectation for future rate changes. As long as the Federal Reserve changes rates according to the market’s expectation, prices and yields are mostly reflected in current prices, prior to any rate changes.

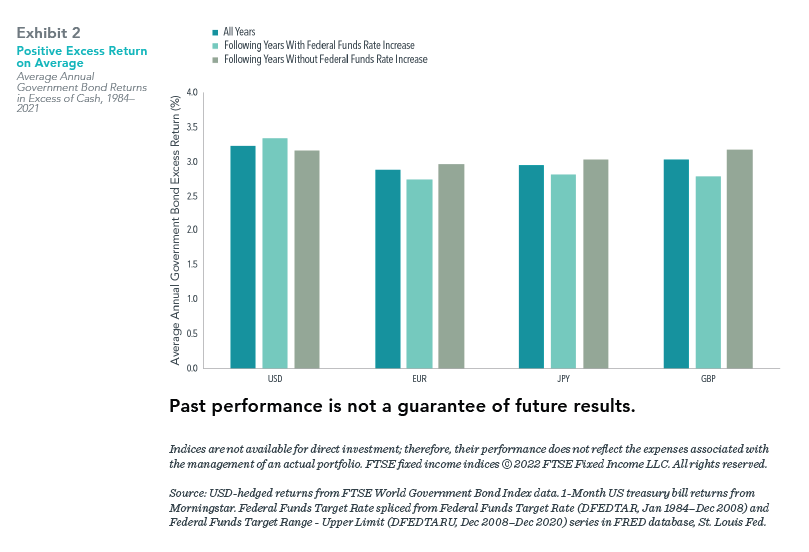

We believe the market is efficient at pricing the available information into current prices, therefore it is challenging to try and time the market. As expected, the chart below shows that there is no correlation between the Federal Funds rate increasing or decreasing and bond returns.

What Happens to Bond Prices When Interest Rates Rise?

Interest rate increases result in short-term pain for long-term reward. At the beginning of 2022, bonds were yielding between 0-2%, but now bonds are yielding 3-5%. As your bonds produce income, you can use that income to reinvest in newer bonds at the higher current interest rates.

The end result? Higher returns. Please see the example below based on a flat yield curve and hypothetical scenarios based solely on mathematical principles.

Scenario 1 assumes a 5-year bond is bought for $100,000 when interest rates are 1%. It assumes the rate stays the same, coupons are reinvested annually, and the bond is continuously reinvested when it matures.

Scenario 2 assumes a 5-year bond is bought for $100,000 when interest rates are 1%. It assumes the rate immediately increases to 4% and stays at 4% indefinitely, again coupons are reinvested annually, and the bond is continuously reinvested when it matures.

As you can see below, scenario 1 increases by exactly 1% each year, while scenario 2 decreases by 13.6% immediately and then increases by 4% each year. By year 5, the wealth in each scenario is the same but by year 20, scenario 2 is $67,262 higher than scenario 1.

|

Years |

Scenario 1 |

Scenario 2 |

|---|---|---|

|

0 |

$100,000 |

$86,385 |

|

1 |

$101,000 |

$89,841 |

|

2 |

$102,010 |

$93,434 |

|

3 |

$103,030 |

$97,172 |

|

4 |

$104,060 |

$101,059 |

|

5 |

$105,101 |

$105,101 |

|

6 |

$106,152 |

$109,305 |

|

7 |

$107,214 |

$113,677 |

|

8 |

$108,286 |

$118,224 |

|

9 |

$109,369 |

$122,953 |

|

10 |

$110,462 |

$127,871 |

|

11 |

$111,567 |

$132,986 |

|

12 |

$112,683 |

$138,306 |

|

13 |

$113,809 |

$143,838 |

|

14 |

$114,947 |

$149,592 |

|

15 |

$116,097 |

$155,575 |

|

16 |

$117,258 |

$161,798 |

|

17 |

$118,430 |

$168,270 |

|

18 |

$119,615 |

$175,001 |

|

19 |

$120,811 |

$182,001 |

|

20 |

$122,019 |

$189,281 |

If you’re still questioning whether investing in bonds is a good idea, remember that bonds serve a key purpose in a long-term investment portfolio because they provide stable income and do not fluctuate in value nearly as much as stocks. For example, even though bonds are down this year, they are still down less than stocks.

If you want to learn more about how bonds can help you reach your personal financial goals, schedule a free consultation with a Wealthstream financial advisor.